When you pick up a generic pill in Germany, France, or Poland, you might assume it’s identical everywhere in the EU. But the truth is more complicated. Behind every generic drug on the shelf is a tangled web of regulatory rules, national bureaucracies, and recent reforms that determine when and where it becomes available. In 2026, the European Union is still struggling to make generic medicines truly uniform across its 27 member states-even though the goal has been harmonization for decades. The 2025 Pharma Package reforms tried to fix this, but they didn’t erase the differences. They just changed how companies have to play the game.

Four Ways to Get a Generic Drug Approved in the EU

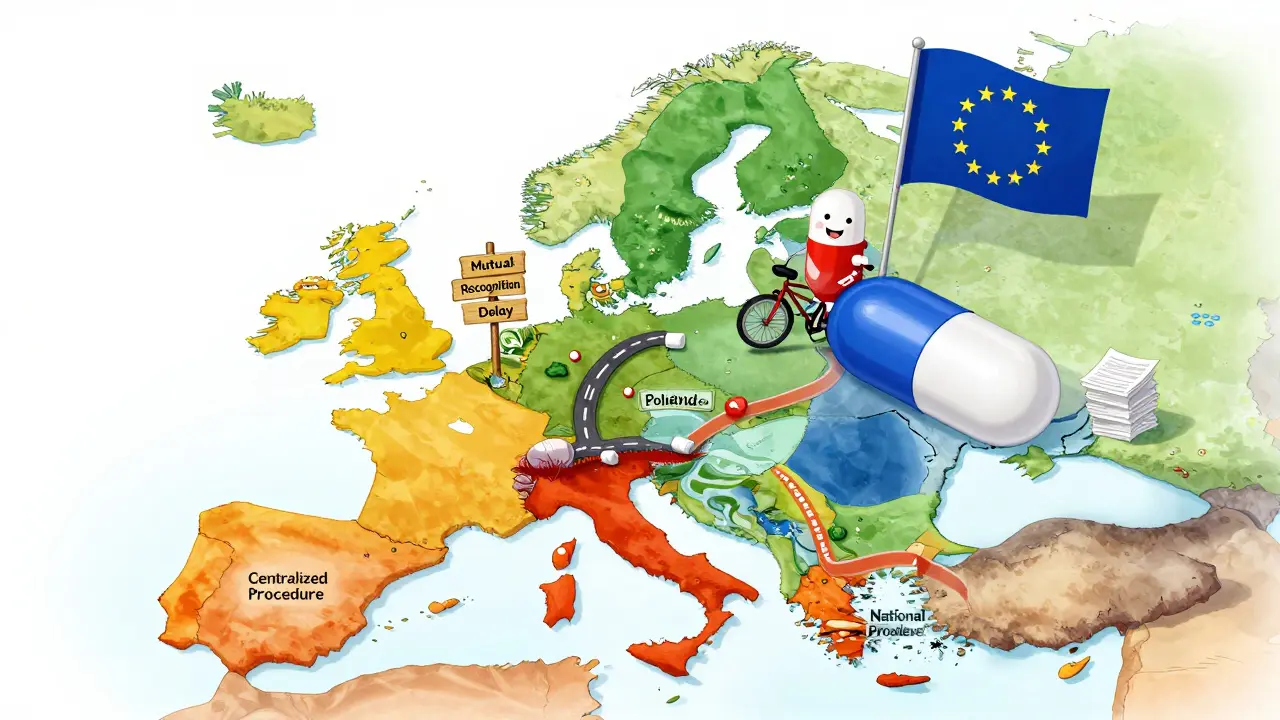

There’s no single path for a generic drug to enter the European market. Instead, manufacturers must choose from four different approval routes, each with its own timeline, cost, and risks. The right choice can mean launching six months earlier-or getting stuck in delays for over a year.

- Centralized Procedure (CP): Submit once to the European Medicines Agency (EMA), get approval valid in all 27 EU countries plus Iceland, Liechtenstein, and Norway. It’s the fastest route for EU-wide access-210 days for assessment, down to 180 days under the 2025 reforms. But it costs €425,000 just in fees, plus another €1.2-1.8 million in consulting and preparation. Only worth it for high-volume generics with projected sales over €250 million. Sandoz used this for its Cosentyx generic and launched across Europe simultaneously in Q2 2025.

- Mutual Recognition Procedure (MRP): Get approved in one country (the Reference Member State), then ask others to accept it. Used in 42% of cases. Sounds simple, but in practice, it’s slow. The official timeline is 90 days for consensus, but real-world delays push it to 132.7 days on average. Teva’s rosuvastatin generic hit Germany first, but Dutch and Belgian markets waited 8.2 months because of pricing delays. The system assumes national authorities will agree-but they often don’t.

- Decentralized Procedure (DCP): Apply to multiple countries at once, with one leading the review. Used for 38% of applications. It should speed things up, but 37% of DCP applications take more than six months due to inconsistent standards. Eastern European regulators sometimes demand extra stability data or different bioequivalence thresholds than Germany or France. This creates a patchwork of requirements that manufacturers have to rework for each country.

- National Procedure: Apply to just one country. Only 5% of applications use this. It’s the slowest-180 to 240 days-and gives you access to one market only. But for companies targeting high-reimbursement countries like France or Austria, it can be a strategic first step. Accord Healthcare found their French national approval took 197 days, while an MRP for five countries took just 142.

Choosing the wrong path can cost millions. A 2025 survey of 47 generic manufacturers found that 68% listed inconsistent national bioequivalence requirements as their biggest headache. Germany, for example, demands extra pharmacodynamic studies for inhalers. France requires detailed pediatric formulation data. One size doesn’t fit all-even if the EU says it should.

What Changed in the 2025 Pharma Package?

The EU’s last major overhaul of generic rules was in 2004. The 2025 reforms were the biggest update in 20 years-and they hit hard. Three changes are reshaping how generics enter the market.

- Expanded Bolar Exemption: Before 2025, generic companies could start negotiating prices and reimbursement only two months before a patent expired. Now, they can begin six months earlier. This might not sound like much, but it’s a game-changer. REMAP Consulting estimates this alone will cut generic launch delays by 4.3 months on average. It gives payers more time to compare prices and forces manufacturers to compete earlier, which could lower prices by 12-18%.

- Shorter Data Protection: The period during which generic makers can’t use the innovator’s clinical data to get approval dropped from 10 years to 8 years, with an extra year of market exclusivity (8+1). If the drug meets public health targets, it can stretch to 10 years again. This means generics can come sooner-but only if they’re not targeting niche drugs with little demand.

- Obligation to Supply: New rules require companies to keep enough stock of essential generics to prevent shortages. Sounds good, right? But critics warn that national authorities are interpreting “sufficient quantities” differently. Some may demand unrealistic stockpiles, forcing smaller firms out. Others might not enforce it at all. Professor Panos Kanavos calls it a “patchwork implementation” that could create artificial shortages in smaller markets.

These changes are already having real effects. Evaluate Pharma projects that generic prescription rates will rise from 65% to 69.2% by 2028. That’s not just more pills-it’s more competition, lower prices, and better access.

Who’s Winning? Who’s Struggling?

The EU generics market was worth €42.7 billion in 2024. Indian companies now control 38% of approvals, up from 29% in 2020. They’re fast, cheap, and good at navigating the messier parts of the system-especially DCP and MRP. Meanwhile, European giants like Sandoz and Viatris hold 52% of the market by value, mostly because they stick to the Centralized Procedure. They pay more upfront, but they win on speed and scale.

Mid-sized companies are caught in the middle. The new Transferable Exclusivity Voucher system gives extra market protection to drugs with over €490 million in EU sales. That’s great for big players-but it’s out of reach for smaller firms. A 2025 EGA analysis warned this could push out European generics that aren’t blockbuster drugs but still serve millions.

And then there’s the paperwork. The 2025 reforms require electronic product information (ePI) in XML format by 2026. That means companies need new IT systems. White & Case estimates this will cost €180,000-250,000 per firm. For a small generic company, that’s a third of their annual regulatory budget.

Why Does This Matter to Patients?

It’s easy to think of generics as interchangeable. But delays in approval mean delays in access. The average gap between a drug launching in the U.S. and in the EU is 22.4 months. Compare that to Canada-just 8.7 months. That’s not just bureaucracy. It’s patients waiting longer for affordable medicine.

Take insulin, for example. A generic version might be approved in Germany by June 2026, but still not available in Bulgaria until November. That’s five months where patients in Bulgaria pay three times more. The 2025 reforms were supposed to fix this. They’ve helped-but not enough.

The EU’s Critical Medicines Act of March 2025 added another layer: mandatory stockpiles of 200 essential generics. This should prevent shortages, but it also adds new testing and verification steps. For some manufacturers, that means more delays. For patients, it means more certainty.

What’s Next? The Road to 2026 and Beyond

The big changes are still rolling out. The expanded Bolar exemption kicked in September 2025. The ePI requirement starts in 2026. The real shock comes on July 1, 2026, when the 8+1 data protection rule fully takes effect. That’s when 78 high-value biologics currently under patent will become vulnerable to generic competition.

Will this lead to more competition? Yes. Will it be smooth? No. The system is still too fragmented. National authorities still interpret rules differently. The EMA provides clear guidance, but a 2025 survey showed 58% of companies found national responses inconsistent-especially on impurity limits for older drugs.

The future of generics in Europe isn’t about one perfect system. It’s about managing complexity. Companies that succeed will be those who invest in deep regulatory expertise, build flexible supply chains, and track national quirks like weather patterns. The EU wants generics to be faster, cheaper, and more reliable. The rules are moving in that direction. But until every country speaks the same regulatory language, patients will still face uneven access.

Why aren’t generic drugs the same price across all EU countries?

Price isn’t controlled by the EU’s approval system-it’s set by each country’s health ministry or insurance system. Germany negotiates prices directly with manufacturers. France uses a reimbursement rate based on therapeutic value. Eastern European countries often pay less due to lower income levels. Even if a generic is approved in all 27 countries, its price can vary by 300% depending on where you buy it.

Can a generic drug be approved in one EU country and automatically sold in another?

Not automatically. Even under the Mutual Recognition Procedure, other countries must review and accept the approval. They can reject it if they claim safety concerns-even if the EMA approved it. This is why a drug approved in France might take six months longer to appear in Poland.

Do EU generics have to be identical to the original brand drug?

Yes, but only in specific ways. They must contain the same active ingredient, in the same amount, and in the same form (tablet, injection, etc.). They must also prove bioequivalence-meaning they deliver the same amount of drug into the bloodstream within 80-125% of the brand drug’s levels. But inactive ingredients (fillers, dyes) can differ. That’s why some patients report different side effects between brands and generics.

Why do some generic drugs take longer to launch in the EU than in the U.S.?

The U.S. FDA has a single approval system. The EU has 27 national regulators plus the EMA. Each country can add its own requirements. The EU also has longer data protection periods (though reduced in 2025) and more complex pricing negotiations. On average, a generic enters the U.S. 13.7 months before it hits the EU market.

Are Indian generic manufacturers dominating the EU market?

They’re gaining fast. In 2024, Indian companies secured 38% of all generic approvals in the EU, up from 29% in 2020. They’re cheaper, faster at navigating complex procedures like DCP, and less reliant on expensive Centralized Procedure filings. But European firms still control more of the high-value market because they focus on complex generics and use the CP for faster, simultaneous launches.

What Should Generic Manufacturers Do Now?

- Map out your product portfolio. High-volume drugs? Use the Centralized Procedure. Niche or low-cost? Try MRP or DCP.

- Start preparing for ePI submission in XML format. Delaying this will block your 2026 launches.

- Build relationships with regulators in key markets. Germany, France, and Italy have different expectations-know them before you apply.

- Use the EMA’s free Q&A portal-but verify every answer with your national authority. Don’t assume consistency.

- Track the 2026 data protection changes. If your drug is nearing patent expiry, now is the time to file.

The EU’s generic system is messy, but it’s evolving. The 2025 reforms didn’t fix everything-but they made it clearer how to win. The companies that adapt fastest will be the ones that bring affordable medicine to patients sooner.

Comments (11)

Maranda Najar

The EU’s generic drug system is a tragicomic opera of bureaucracy, where a life-saving pill can be held hostage by five different ministries, each with their own spreadsheet of arcane requirements. I’ve seen patients cry because their insulin was approved in Berlin but not in Bucharest-five months later. This isn’t harmonization. It’s a Kafkaesque labyrinth built by bureaucrats who’ve never held a prescription in their hands. The 2025 reforms? A Band-Aid on a hemorrhaging artery. We need one regulator. One standard. One system. Not 27 different versions of ‘almost the same thing.’

Christopher Brown

America does it right. One FDA. One approval. One price. Europe’s mess is why generics cost more here. Stop overregulating. Just approve the drug and let the market decide.

Sanjaykumar Rabari

This whole system is a scam. Big pharma and EU bureaucrats are in cahoots. The real reason Indian companies are winning is because they’re not paying bribes. The ePI requirement? A cover to force small firms out. The stockpile rules? A way to make you buy from the right companies. I’ve seen the documents. They’re hiding something.

Kenzie Goode

I just want to say-this is heartbreaking. I work in public health, and I’ve watched patients choose between rent and their meds because a generic wasn’t available in their country. The 2025 reforms were a step, but they didn’t go far enough. We need a central database of national requirements, real-time updates, and mandatory transparency. Not just for companies-but for patients. They deserve to know why their medicine is delayed. This isn’t just policy. It’s human suffering wrapped in regulatory jargon.

Dominic Punch

Let me break this down for anyone still confused. The Centralized Procedure isn’t just ‘expensive’-it’s strategic. If you’re launching a high-volume drug, paying €2M upfront saves you 6 months of chaos. The MRP? A nightmare if your Reference Member State is Italy-bureaucrats there take 90 days just to open your email. I’ve seen companies waste a year because someone in Poland demanded extra stability data for a drug approved in France. The 2025 reforms? They didn’t fix the system. They just made the paperwork prettier. Your move: map your portfolio, know your regulators, and never assume consistency. The EMA says one thing. A national authority says another. Always verify. Always double-check. Always document.

Khaya Street

Honestly, I don’t get why this is even a debate. The EU should just copy the U.S. system. Simpler. Faster. Cheaper. All this national nonsense is just a way for governments to feel powerful. Meanwhile, people die waiting for insulin.

Christina VanOsdol

OMG. I just spent 3 hours reading this. 😭 The ePI requirement alone? 💥 That’s a $250K hit for small firms. And don’t even get me started on the ‘bioequivalence thresholds’-why does Germany need extra pharmacodynamic studies for inhalers??? 🤯 This isn’t science-it’s a regulatory scavenger hunt. And India’s winning? Of course they are. They’ve got teams of 20-year-olds in Bangalore working 18-hour days to navigate this madness. Meanwhile, European firms? Still using Word docs in 2026. #GenericsAreNotEqual #RegulatoryNightmare

Brooke Exley

Look-I know this sounds dry, but this is life-changing stuff. Every delay in approval means someone’s grandfather can’t afford his blood pressure med. Every inconsistent standard means a teenager in Romania gets a different pill than her sister in Berlin. The 2025 reforms? They’re not perfect-but they’re a start. What we need now isn’t more rules. It’s empathy. We need regulators who’ve sat with patients. Who’ve seen the receipts. Who’ve held a bottle of insulin and thought: ‘This should be cheaper.’ The EU isn’t broken. It’s just forgotten who it’s supposed to serve. Let’s remind them.

Alfred Noble

so like... the centralized procedure is only worth it if you're selling over 250 million? lol. that's wild. i thought generics were supposed to be cheap. guess not. also epi in xml? ugh. my company's it team is gonna lose their minds. btw i think the indians are winning because they don't care about fancy packaging. just get the pill out. 🤷♂️

Matthew Brooker

The real win here is that generics are hitting 69% prescription rates by 2028. That’s millions of people getting affordable meds. The system’s messy, sure. But progress isn’t pretty. It’s slow. It’s full of exceptions. It’s national quirks and bureaucratic tangles. But it’s happening. Keep pushing. Keep filing. Keep adapting. The patients are counting on us.

Emily Wolff

This is why Europe will never lead in pharmaceuticals. Too many cooks. Too many rules. Too much ‘careful consideration.’ The U.S. and India are moving forward. Europe? Still debating whether a tablet should be blue or white.